Garden Indices

A market-cap weighted index assigns weights to assets proportional to their market capitalization relative to the total market capitalization of the portfolio (or basket). Here’s a structured overview of market-cap weighted indexes, based on the content of the document you uploaded.

1. Concept of Market-Cap Weighting

A market-cap weighted index assigns weights to assets proportional to their market capitalization relative to the total market capitalization of the portfolio (or basket).

Formula:

This ensures that larger companies or tokens (by market value) exert more influence on the index.

2. Steps in Construction & Rebalancing

-

Gather Data

- Market capitalization of each asset.

- Current dollar value held.

- Asset prices.

- Total portfolio value.

-

Calculate Target Weights

- Divide each asset’s market cap by the sum of all caps.

- Example: If A = 500B, B = 300B, C = 200B → weights = 50%, 30%, 20%.

-

Compare to Current Holdings

- Identify deviations between current and target values.

-

Rebalance When Needed

- Sell overweight assets, buy underweight ones.

- Match buy/sell so there’s no net cash flow.

- Trade in whole shares/tokens.

3. Tolerance & Cost Efficiency

-

Tolerance threshold: A set percentage (e.g., 5% of portfolio value) defines when trades are triggered.

- Small deviations below threshold are ignored (avoids over-trading).

- Example: On a $20,000 portfolio with 5% tolerance ($1,000), trades are only executed if deviations exceed $1,000.

-

Transaction cost minimization:

- Fewer trades = lower fees.

- Batch trades if managing multiple accounts.

- Consider bid-ask spreads for cost/benefit.

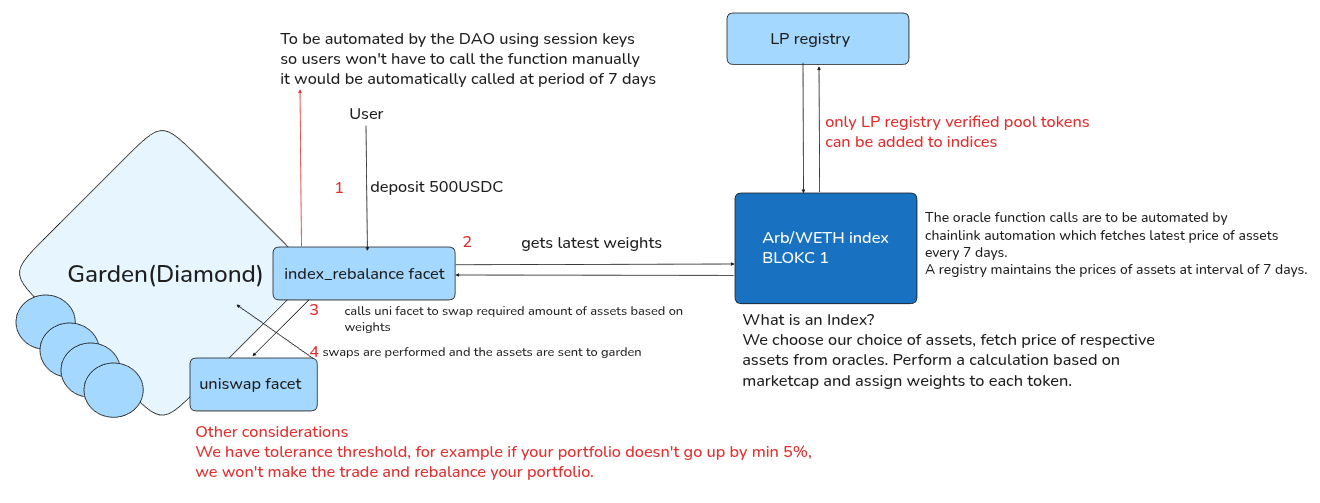

Proposed architecture(WIP)

Trade samples

Let’s work through three illustrative scenarios with WETH and ARB, where we compare target weights vs. calculated (current) weights under a 5% tolerance rule.

Assumptions

-

Portfolio Value = $10,000

-

Asset Prices:

- WETH = $2,000

- ARB = $1.00

-

Target Weights:

- WETH = 70%

- ARB = 30%

-

Tolerance: +5% of total portfolio value ($500) — swaps are performed only if they improve the portfolio value by at least this much.

Case 1: Target weight = Current weight → No swap

-

Current holdings:

- WETH = 3.5 ($7,000 value, 70%)

- ARB = 3,000 ($3,000 value, 30%)

-

Current weights = Target weights (70/30).

Action: No swap required. Portfolio is aligned with targets.

Case 2: Target weight higher → Swap performed

Suppose current portfolio is:

- WETH = 3 ($6,000, 60%)

- ARB = 4,000 ($4,000, 40%)

- Current weights: WETH 60%, ARB 40%.

- Target: WETH 70%, ARB 30%.

To rebalance:

- WETH target = $7,000. Currently $6,000 → need +$1,000 WETH.

- ARB target = $3,000. Currently $4,000 → need –$1,000 ARB.

Swap $1,000 ARB → WETH.

-

Post-swap:

- WETH = $7,000 (70%)

- ARB = $3,000 (30%).

Value shift = $1,000 > $500 tolerance → Swap executed.

Case 3: Target weight higher, but below tolerance → No swap

Suppose current portfolio is:

- WETH = 3.3 ($6,600, 66%)

- ARB = 3,400 ($3,400, 34%)

- Current weights: WETH 66%, ARB 34%.

- Target: WETH 70%, ARB 30%.

To rebalance:

- WETH target = $7,000. Currently $6,600 → need +$400 WETH.

- ARB target = $3,000. Currently $3,400 → need –$400 ARB.

Swap size = $400.

- This is < $500 tolerance, so no swap performed.

- Portfolio remains slightly off-balance but within acceptable bounds.

Summary

- Case 1: Perfectly aligned → no action.

- Case 2: Significant deviation → swap performed.

- Case 3: Deviation exists but below tolerance → no action.

This architecture is still under development and will be introduced in a future release. The information provided here is preliminary and may change without notice.